3 ways to save more without spending less

Contents

Singapore is an expensive city – the most expensive city in world, in fact, according to the Economist Intelligence Unit. In a 2015 survey, 87% of 2,000 Singaporean participants reported that they have had to make financial compromises due to the rising cost of living.

If you’ve been cutting on spending but still feeling the pinch, you’ll want to make use of cashback and money-saving tools that will allow you to save more without spending less.

In order to get the most out of your spending, it’s best to make use of tools that require little effort and can integrate seamlessly into your spending habits. Here’s a fuss-free guide to saving more without spending less in Singapore:

Use cashback and money-saving tools

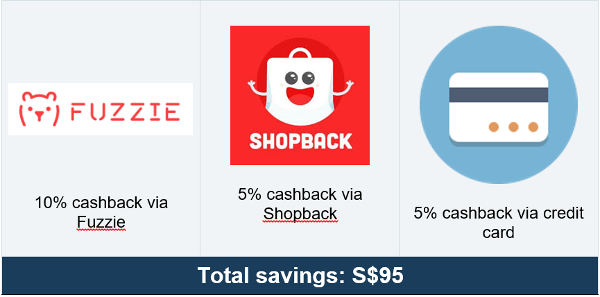

1. Cashback credit card

To the uninitiated, it may seem odd to think of a credit card as a money-saving tool, rather than an instrument to borrow money at high interest rates. However, careful use of a credit card has plenty of advantages: it can help you save significantly, accumulate air miles to redeem free flights and improve your credit score.

A cashback credit card helps you save money through its cashback or cash rebate feature, whereby a percentage of the purchase amount is returned to you. In Singapore, you can find credit cards that give less than 1% all the way to 10% cashback.

However, you’ll need to read the fine print – the amount you can redeem may be subject to limitations, like a monthly cashback cap or a minimum monthly spend. Your credit card may also have a base and an additional cashback amount, in which you may only be entitled to the additional cashback amount if you hit the minimum monthly spend.

Here are a few credit cards with some of the highest cashback rates in Singapore for popular categories of spending:

Hitting the minimum spends for the credit cards above should be achievable by billing your regular spending (petrol, bills, groceries, etc.) to your credit card.

If the minimum monthly spending is still out of your reach, these two cards offer 1.5% cashback without a minimum monthly spending or a monthly cashback cap:

- Standard Chartered’s Unlimited Cashback Card

- American Express True Cashback Card

The unlimited cashback credit cards are also great if you are planning some big purchases. For example, if you are furnishing a new home, you can use your unlimited cashback card for your spending.

By spending S$15,000, you will receive a cashback of S$225. Of course, you will need to ensure that you have the ability to repay the full amount so you won’t incur any interest charges.

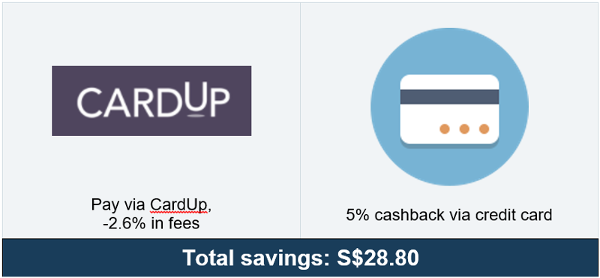

2. CardUp

To maximise your cashback rewards or redeem more air miles on your credit card, you’d want to bill large payments to your credit card (assuming you have enough cash to repay your credit card debt, of course). However, many large, recurring payments (like your rent) can’t be paid through credit cards.

Here’s where CardUp comes in. This local startup allows you to make big payments by credit card, even to recipients that don’t accept them. CardUp processes your credit card payment and delivers it to your recipient by electronic bank transfer, so your recipient won’t need a CardUp account to receive your payments.

Currently, CardUp’s service supports:

- Rental payments (to a landlord)

- Rental deposits (to a landlord)

- Condominium maintenance fees (to a MCST or property developer)

- Tuition/School fees (to Singapore-based schools or education centres)

- Insurance premiums

- Income tax

CardUp charges a 2.6% fee for each transaction, with a minimum fee of S$3.40 for payments of S$130 or less. This may seem like a high amount, especially considering that your credit card may offer a cashback amount that’s not much higher, but the savings can add up over the year.

Here’s an example of how much you can save with a credit card that offers a 5% cashback:

If you have other large monthly payments but have already hit the cashback limit on your credit card, you can consider getting another credit card to maximise cashback rewards – provided you have the cash to cover all credit card debts .

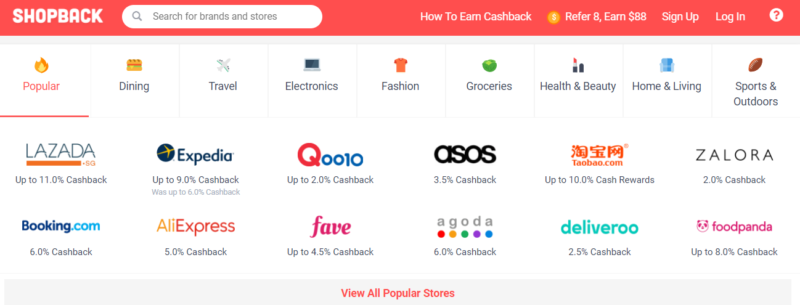

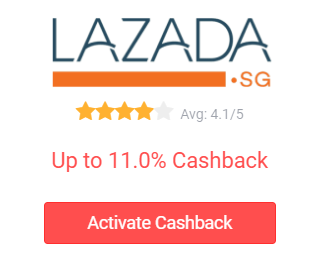

3. ShopBack

ShopBack is a website that offers a cashback percentage if you purchase goods and services through its links. They have tons of popular merchants, like Lazada, Zalora, Taobao, Agoda and more, with cashback rates around 1.5% to 11%. It’s an easy, 3-step process to getting your cashback:

-

- Visit https://www.shopback.sg

- Choose an online shopping merchant

- Access the merchant through the “Activate Cashback” button and browse the site as usual

The cashback you earn will be credited to your ShopBack account, which you can then cash out.

4. Fuzzie

For cashback rewards on both online and offline purchases, Fuzzie fits the bill. They offer over 100 brands, including Topshop, honestbee, Lazada and Zalora. You’ll just need to go through a few steps to get instant cashback, ranging from 5% to 30%:

- Choose an e-gift card for your selected brand. You buy gift cards that cost as little as S$5, all the way to S$100.

- Checkout and receive cashback. Once you’ve purchased your gift card, you will receive a cashback amount in your Fuzzie account. You can cash it out or use it for your next Fuzzie purchase.

- Redeem your gift card. Your gift card will come with a promo code that will work with online or offline stores!

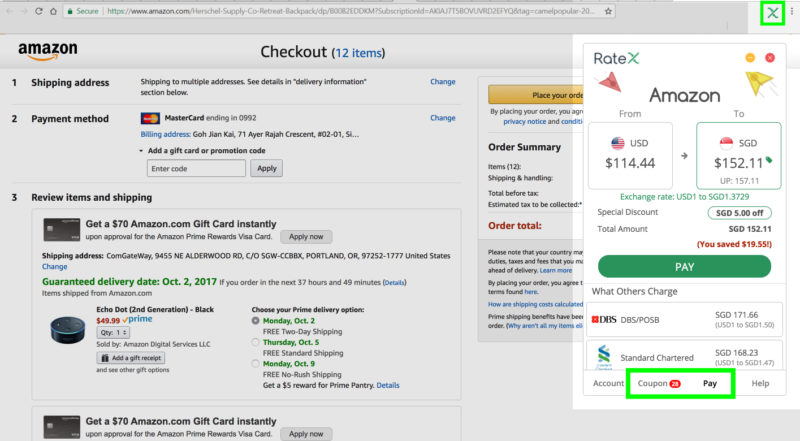

5. RateX

If you’re buying online from overseas merchants like Amazon and Taobao, use RateX’s browser extension to save on currency conversion rates. RateX will search for the best exchange rates at checkout, and automatically apply any available coupon codes (for both international and local shopping sites!). Best of all, RateX doesn’t charge any fees.

Image from RateX.com

Take advantage of petrol loyalty programmes

Loyalty programmes can seem enticing at first…until you’re at the checkout counter, rummaging for a card that hasn’t seen the light of day since you applied for it a few months ago.

Keeping track of these programmes can be a hassle, and its rewards may be too insubstantial to be worth the effort – that’s why we recommend only signing up for loyalty programmes that provide significant savings (like a frequent flyer programme), or for those whose products and services you regularly spend on.

For this reason, signing up for a petrol loyalty programme may be worth the hassle. If you own a vehicle in Singapore, you might be spending a sizeable fraction of your salary on petrol. Taking advantage of a petrol loyalty programme will allow you to save on a service that you use often.

Stack them up

Using any of the tools above will net you some pocket change, but stack them together and you’ll be seeing significant savings.

Here are a few examples of how you can stack these tools:

1. Paying an annual insurance premium (S$1200)

2. Online shopping with Lazada (S$500 bag)

3. Accommodation booking via Agoda (S$1200)

4. Paying for petrol (30 litres of 95-Octane x S$2.23 per litre = S$66.9)

As you can see, your potential savings can snowball into pretty big amounts. That’s a lot of dough for very little work.

Originally written by Jen-Li Lim

This post was first published on iMoney, a platform that empowers consumers to make intelligent decisions on money matters.